America Is Fast Becoming a Nation of Debt and Debtors (and Tim Walz's Jobs Record)

Americans need to change from being an instant gratification society based on debt to a delayed gratification country based on savings. Otherwise, parallels to the fall of Rome won’t be theoretical.

I abhor debt. As a high schooler, my oldest brother had me read M. Scott Peck's “The Road Less Traveled: A New Psychology of Love, Traditional Values, and Spiritual Growth” which preached the concept of delayed gratification. Even though the book was a pop psychology book, the section on delayed gratification hit home for me, as it defined that term as “a process of scheduling the pain and pleasure of life in such a way as to enhance the pleasure by meeting and experiencing the pain first and getting it over with. It is the only decent way to live.” The concept just made sense to me.

As a recent college graduate in law school in 1996, I read Thomas Stanley’s and William Danko’s book, “The Millionaire Next Door: The Surprising Secrets of America’s Wealthy,” when it first came out. I re-read the book every five years to remind myself about the lessons highlighted in the book. As my kids can attest to given how often I drone on about those lessons, one of the keys to life is consciously NOT trying to keep up with the Joneses because, in all likelihood based on the extensive research, the Joneses are neck-deep in debt so you shouldn’t confuse their trappings of wealth (big houses, luxury cars, brand label clothes, and exotic vacations) with actual wealth. The vast majority of the Joneses might make a lot of money every year, but their lifestyles require them to spend that money and then some via credit, so their actual net worths (assets minus liabilities) are zero or negative.

Since those books were written, America and Americans have gotten far too comfortable carrying debt due to the ubiquity and ease of obtaining credit—whether that credit comes in the form of a card, home mortgage, car loan, student loan, or line of credit. Delayed gratification has been replaced by instant gratification. You want a $1,200 iPhone? Whip out the credit card. You want a new car every few years? Take out loans. You want a Louis Vuitton bag? No problem—just swipe the plastic. You want to vacation like a king? Charge it. I know too many people who have five-to-six figures of credit card debt (along with car, mortgage, and/or student loan debt) who willingly add to that debt knowing full well they will never pay it off so will die in debt, thereby shifting their instant gratification lifestyle debt onto the rest of us (i.e., we all pay more for credit because the credit companies account for debt they won’t collect via higher annual fees and credit rates).

With Joe Biden’s unconstitutional student loan forgiveness program, we’ve all read about the people who took out federal student loans to acquire worthless degrees in things like womyn’s studies, English literature, and other liberal arts degrees in which the jobs are scarce and pay very low. When people started to take out car loans covering the new car they can’t afford that they are currently driving, as well as the old car they traded in for that new car that still had debt attached to it, you know we are reaching a very dangerous tipping point.

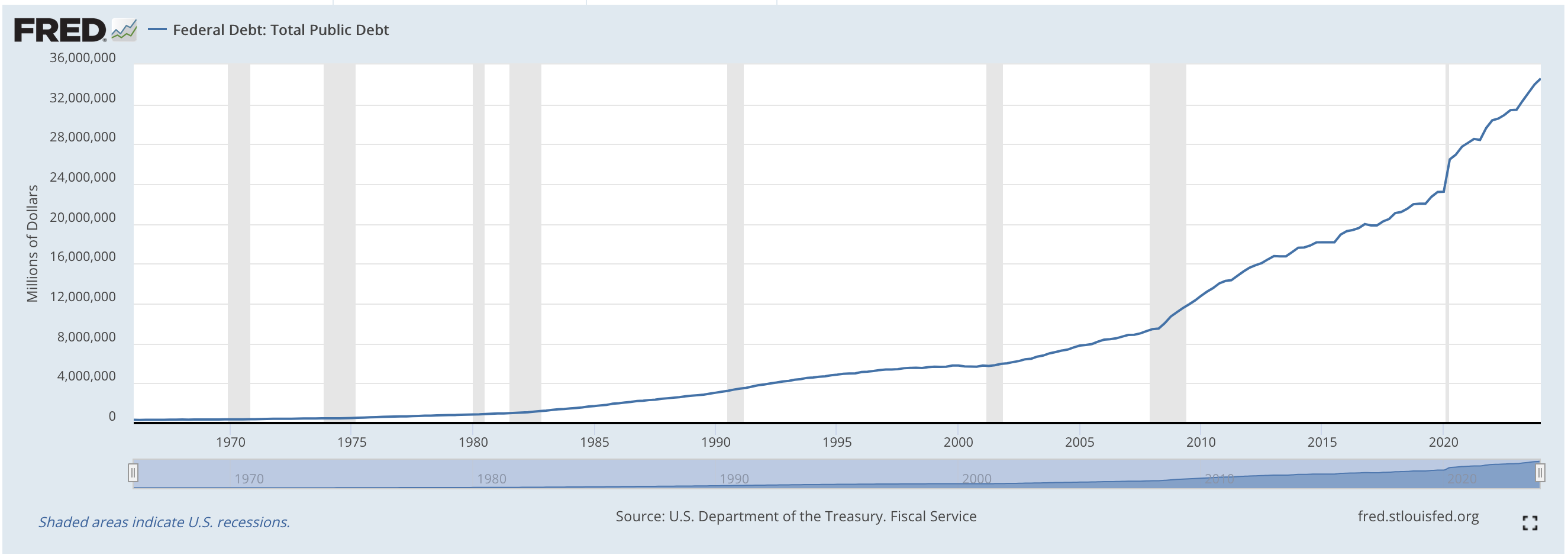

According to the Federal Reserve, total national debt as of January 2024 sat at $35 trillion. That enormous debt is generating annual interest payments of $1.1 trillion (and going higher). To put that figure in perspective, servicing that annual interest payment alone (i.e., doesn’t put a single dollar towards reducing the national debt) will swallow 76% of all income taxes paid by Americans, which leaves just 24% of income taxes to cover the rest of federal spending that isn’t more deficit spending that adds even more to the national debt. The explosion of federal spending since 2000 is truly astonishing. As noted:

At the turn of 21st century, the national government debt was $5.77 trillion, and by 2010 it had more than doubled to $12.77 trillion. The debt reached $23.22 trillion at the beginning of 2020. And only a few years later on Biden’s watch, it now surpasses $35 trillion.

This explosion isn’t a Democrat or Republican problem. It is a Democrat AND Republican problem, as each party controlled the federal government for exactly twelve years since 2000 (eight under George W. Bush with four more under Donald Trump versus eight under Barack Obama along with just about four under Biden). It only gets worse when you factor in all federal debts, liabilities, and unfunded federal obligations.

Based on data from a U.S. Treasury report, the federal government has amassed $142 trillion in debts, liabilities, and unfunded obligations. This staggering figure equals 93 percent of all the wealth Americans have accumulated since the nation’s founding, estimated by the Federal Reserve to be $152 trillion.

…

The primary components of this burden, which are unpacked below, include:

• $26.3 trillion in publicly held national debt.

• $16.6 trillion in liabilities that are not accounted for in the publicly held debt.

• $104.2 trillion in unfunded social insurance obligations.

These figures tally to $147.1 trillion in debts, liabilities, and unfunded obligations. Offsetting this is $5.4 trillion in commercial assets owned by the federal government, leaving a grand total shortfall of $141.7 trillion.

This level of debt equates to a debt of $432,252 for every American alive today or $1,098,087 per household. Both Medicare and Social Security are just a few years away from running out of money to pay obligations those programs have incurred. Someone will have to pay the piper by getting less from those programs than they were promised and/or having to pay higher taxes to meet the promises made.

This debt creates a viscous cycle. The federal government prints money to cover deficit spending that adds to the national debt and interest payments on that debt. The printing of money causes inflation and interest rates to go up, which increases prices on goods and services across the economy. Higher inflation results in wages and salaries failing to keep up with rising prices on goods and services, thereby forcing consumers to spend more for less. Americans then are required to pay higher credit rates on cards, home mortgages, and car loans to maintain their instant gratification standard of living. When consumer spending tappers off due to inflation and debt, the economy goes into a recession. To “help” those Americans who can’t keep up due to both tough luck and an instant gratification lifestyle and to pull the country out of a recession, the federal government prints and spends more money on more and bigger government programs in order for those in charge to keep their popularity and get reelected.

Rinse and repeat.

This vicious cycle won’t end well. At some point, America will not find buyers for its debt, the dollar will lose value, and hyperinflation like seen in Argentina will crush America and most Americans. Our profligate spending creates national security issues, as well. Our enemies like the Chinese government hold a lot of our debt that they could cause enormous economic problems should they demand payment or stop buying our debt. There are only two ways to stop this madness: (1) rein in federal spending and (2) return to being a delayed gratification society.

If you can’t pay cash for something or pay the credit card in full each month, then you shouldn’t buy or do it. Save for it like Americans used to do. At some point, America and Americans need to change from being an instant gratification society of debt and debtors to a delayed gratification country of savings and savors. Otherwise, parallels to the fall of Rome won’t be theoretical.

P.S. For those wondering about how Minnesota’s private sector has done under Governor-now-vice-presidential-candidate Tim Walz, see the charts below.